Bonds

When I think about financial plans and strategies, I try to place disproportionate energy on the BIG things that can derail our plans.

In the world we live in, reward almost always requires risk. So we should want to take risks, but we should also want to avoid risks that carry a downside which is SO bad that it prevents us from being able to take future risks. This is why I preach diversification — so that one single holding can’t adversely impact your plan in a negative way— and it’s why we’d never play Russian Roulette… despite the 1/6 chance of a negative outcome, the negative outcome is SO bad that we can’t take that risk no matter how good the potential upside could be.

With the way we advise investors’ portfolios, the risk of catastrophic failure is significantly mitigated by broadly diversifying portfolios across markets. We know markets tend to rally, pull back, recover, then repeat — so I’m not as worried about them.

However, I tend to hear a lot of concern about the federal budget deficit and ballooning national debt. I’m concerned too, because large systemic problems have the potential to disrupt even broadly diversified portfolios. So I’ve been spending a lot of time on this lately, particularly over the last two weeks reading, researching, and evaluating some alternative theories which may shed some light on the issue.

Enjoy,

Adam Harding, CFP

Disclaimer:

Diversification does not prevent loss or guarantee returns. It does, however, prevent you from owning a bunch of one single investment and then seeing that investment’s price get destroyed along with your financial future.

The Deficit (and WW2)

The response by the federal government to the COVID-19 pandemic has taken us back to levels of debt not seen since World War II — the below chart of US Debt to GDP highlights this relationship.

Not good, right? Particularly as we consider the projection at the right of the chart.

No, it’s not, but nearly everyone else is in the same boat (see below), although it still may seem like we’re nearing a crisis.

So what happens when debt rises to ‘crisis’ levels?

Well, let’s first define what a debt crisis is… In the simplest terms, the culmination of a debt crisis occurs when investors no longer want to own a country’s debt because they think they may not get paid back. Given the above, we can see that our domestic trend is in line with a global trend in many different countries, so on a relative basis we’re not as poorly positioned as it may appear.

But like anything else in the markets, debt crises are very difficult to predict. However, I don’t believe we’re nearing that situation in the US anytime soon.

In fact, I’d encourage us all to consider a slight change in verbiage:

Reconsider the term The National Debt and change it to The National Investment.

That’s really what this kind of debt is (or at least what it’s supposed to be), an investment.

It’s hard for us to think about debt this way — after all, no one would ever consider personal debt like a credit card or auto loan to be an investment. We’ve been appropriately conditioned to think of debts as an additional mouth to feed, or a vacuum which sucks away our ability to save and invest for something bigger. But the National Debt is actually being incurred as a result of trying to accomplish something bigger via government spending. This is why it’s effectively an investment (despite how poorly utilized it often is).

In this case, the important thing is that the investment is ROI (return on investment) positive — meaning that the cost of the debt (interest) is lower than the returns on the debt (GDP growth). If those conditions are met, it’s often a good investment.

So as you consider policy proposals and hear about plans to spend $_______ Trillion dollars or whatever, remember to ask yourself and the proponents of the policy about the ROI potential.

However, not everyone believes that the deficit matters — notably, many of the politicians with BIG multi-trillion dollar agendas who believe in Modern Monetary Theory (MMT).

MMT proclaims that most countries who issue their own currency face no financial constraints other than hyperinflation or currency debasement. Thus, for many governments — including the U.S. — there is no risk of default. Rather than saying “how much tax revenue did we receive?” and then creating a shopping list to spend those funds, the government can decide what they need to spend as their first priority, and then address financing through taxation and debt issuance.

To better understand Modern Monetary Theory from one of its biggest supporters, over the last two weeks I read The Deficit Myth by Stephanie Kelton.

It’s an interesting read from an economist whose views differ significantly from my own — many of which I now believe are correct (and some which I think are still far-fetched).

In the book, Kelton explains that inflation is evidence that a deficit is too big, while unemployment is evidence of a deficit that is too small. She claims that the large deficit isn’t a concern because we could effectively just issue the currency to pay it off with a few clicks of the keyboard and mouse. Thus, under MMT, fiscal policy (i.e. where funds are directed) plays a more central role in the management of inflation. But that also means politicians would be more critically involved in establishing the environment and how impactful inflation can be.

As a side note, the fiscal policy element of MMT isn’t something I’m necessarily comfortable with — I prefer a market-based system and don’t necessarily trust politicians to guide the economy; the evidence is pretty clearly against that kind of consolidated power.

See, on one hand, MMT solves the worry about the deficit, but on the other hand it grants more power to policymakers — and as a believer in the invisible heart of capitalism, I like the market-based approach with the Federal Reserve acting as a mediator of the money supply.

Speaking of the Federal Reserve. Let’s touch on their role going forward. The Fed’s dual mandate of hitting an inflation target and maximizing employment actually kind of sounds like the balancing act required with MMT. In short, these schools of thought may actually not be too far apart. In both cases, the deficit is manageable as long as GDP growth remains a focus and inflation is kept in check.

Still, the government’s response to COVID-19 should be watched carefully as the National Debt is concerned — the “investment” made is not one which should help GDP growth in a meaningful way. Instead, this was more about crisis management than national investment. Some of that stimulus will certainly help grow the economy, but increased productivity is not being a widely communicated byproduct of the congressional action.

This leads me to the next point: inflation as deficit/debt risk.

These days I get more questions about inflation than anything else, and I don’t blame anyone for being concerned about it — everything has gotten more expensive and inflation is definitely here.

But do you know who doesn’t care as much about inflation? Investors who’ve captured returns over the last decade to help grow the purchasing power of their dollars.

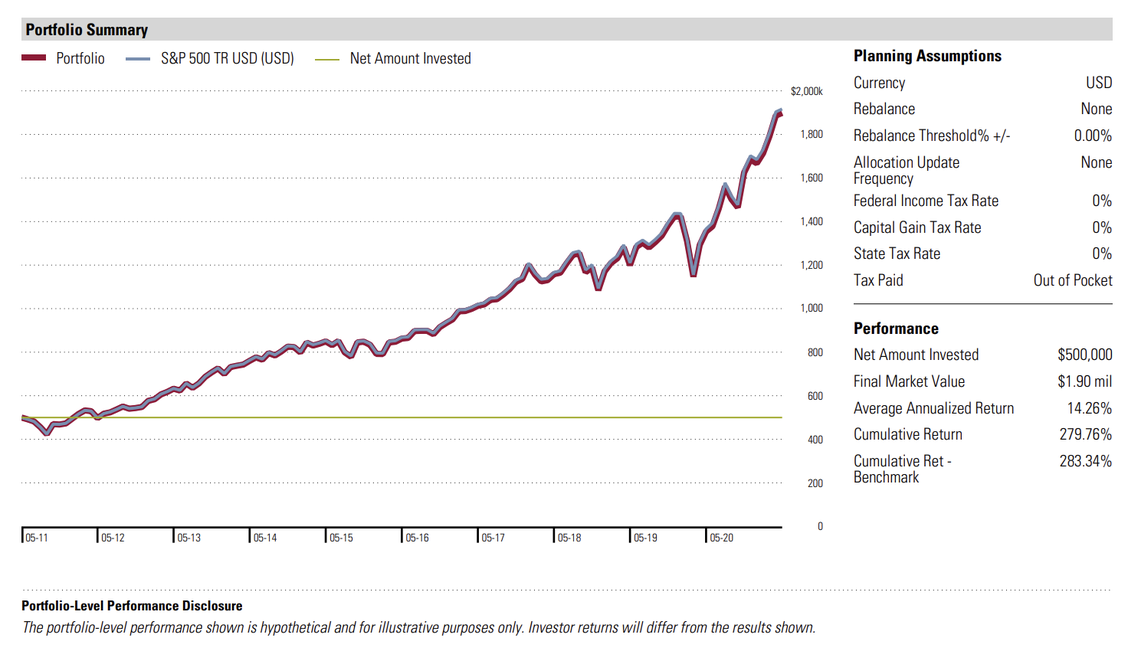

Below is a hypothetical $500,000 investment made 10 years ago into an S&P 500 ETF (symbol SPY) in May 2011 and held through May 2021.

As you can see above, this hypothetical $500k investment reaches nearly $1.9m over 10 years after seeing a 14.26% average annual return. If this was your experience for a decade then suddenly inflation seems to be much more of an afterthought, right?

*Let me reiterate that this is a hypothetical investment and not a client of mine. I launched the firm in 2016 so it would be impossible to track back to 2011, but the lesson remains useful.

This example highlights two things for me:

1) I don’t think a 14% annualized rate of return is probable for the next 10 years… Best to taper expectations, plan around lower expected returns, then be happy if you do better than expected.

2) There were A LOT of reasons to sell along that 10 year period above: 2 elections, a bunch of Presidential Tweets, countless doomsday predictions, terrorist attacks, a global pandemic, geopolitical conflicts, a Trade War, etc etc etc…. Not allowing those things to impact an investment plan is a difficult but essential skill.

So let’s tie these two things together…

If the deficit and national debt are in fact investments and the downside of those investments is that there may be inflation, then we have to consider how to keep up with inflation.

Stocks have been historically great at keeping pace with inflation. The downside = volatility. You have to be willing to ignore the reasons to sell.

Real estate has also been historically great at keeping pace with inflation. If you participate in privately held real estate, then the downside is illiquidity (i.e. not being able to quickly and easily turn the investment into cash) and high transaction costs. If you buy real estate in a mutual fund or ETF then the primary downside is similar to the downside of stocks; volatility.

Bonds are not great inflation hedges, particularly with low current interest rates. A bond pays a stated interest rate and as an example, let’s say a bond pays 3.5% per year. Well if inflation is higher than expected, then that fixed 3.5% looks more unattractive than it did before there was inflation (3.5% now buys less stuff for the bond holder)

Also, one way the Federal Reserve can attempt to stave off inflation is to increase interest rates, which encourages saving in lower risk investments like high yield savings, CDs, etc.. More saving = less dollars attempting to be spent on stuff = less inflation. But increasing interest rates means that the old bonds which were issued with lower rates are now not as attractive as the new ones with higher rates, so the price of the old bonds drops. So if we think interest rates are going to rise, then bonds are not as enticing as both a store of value and an inflation hedge.

Commodities can be a good inflation hedge, but it can be hard to guess which ones will win and which won’t. Gold is having a subpar year compared to many commodities, while energy, corn, and timber are seeing significant appreciation… This is a difficult guessing game. Still, when it looks like stuff can get more expensive in the future it can make sense to want to buy a bunch of it right now. And unless you have a giant pantry for storing corn and soybeans, the commodities markets may provide a way to gain exposure.

With that said, I think stocks and real estate have the potential to provide enough of an inflation hedge but with the added benefit of also producing yield (dividend or rental income) unlike commodities which investors can only benefit from if there is an increase in price.

So here’s the thing:

Surviving the next cycle as an investor is going to require a lot of guts and the ability to stick to a longer term plan. There’s not a magic low volatility investment which also has the potential to beat inflation handily, there are only the tools we have at our disposal along with an understanding of reality of the situation we’re in. Someone will tell you this is untrue and that there is some amazing alternative approach which is usually only available as a result of the product they sell... It will be hard, but try not to listen to them.

There are a few subtle things I can do (which I am doing in many cases) from a portfolio design standpoint, but they aren’t magic formulas. If you’d like to discuss some of these tweaks and design elements, just contact us and we’ll talk about it.

Lastly, as the response to COVID has presented us with Debt-to-GDP levels not seen since WW2, I’d like to leave you with below observation.

At the time of Pearl Harbor, the U.S. artillery was 75% horse drawn. Yes, HORSES carried most American artillery.

By the end of the war we had nuclear weapons.

Think about that pace of innovation for a minute… When we come together for a collective cause we can achieve an astonishing amount of progress in a very short amount of time. We saw this in our war effort and we’ve seen this in the development of COVID-19 vaccines in record time.

Only time will tell what will be the byproduct of this point in history.

That’s all for now.

Onward,

Adam Harding | CFP | Advisor | Owner @ Harding Wealth Inc. | Smartvestor

Mobile Number: 480-205-1743

Copyright (C) 2021 Harding Wealth, Inc. All rights reserved.