Recovery

A client asked me this morning, “Adam, my husband and I are both 70 years old, will we ever recover from this drop?”

It’s a good, normal, perfectly human question, and, in environments like this, the thing all of us want is certainty.

This is super understandable and I would give anything to know exactly when things will turn around and when the recovery will occur, but that’s not how this machine works. This machine rewards patience, discipline, and the acknowledgment that uncertainty is why investors have been handsomely rewarded, historically.

But still, when answering questions like will we recover, I first tend to revisit the financial plan we have in place.

Are your cash needs met?

Do you have any big upcoming changes?

Are your loved ones in a good position? etc.

The markets are full of irreducible uncertainty, so I can’t dive too deep into my own prognostications of what I think will happen (believe me, I have a lot of good guesses… But that’s just what they are, guesses). Instead, I frame it like this:

Individual companies are not immune from getting knocked down and staying down, but the Stock Market as a whole has recovered from every other historical challenge, I don’t see any reason why this would this be any different. This is why we stay diversified and why we stay the course.

But really, think about our past challenges — the disasters endured and those we dodged — and it will hopefully build some confidence that things will be okay; especially considering how many of the past circumstances were far more dire than today’s environment.

See for yourself; here is 35 years of utter chaos along with the global stock market:

So, yea, the market has been resilient and rewarding, but I know that doesn’t help with out psyche the short term, so…

Just for the heck of it, let’s talk about market recovery in each of the last two BAD stock market routs.

Scenario #1: The Tech Bubble

For those of you less familiar with the Tech Bubble, here’s the super short explanation of what happened:

From 1995-2000, the tech-heavy NASDAQ index rose by more than 400%.

The rise was largely the result of euphoria around the potential of the internet and the companies at the forefront of the information-age revolution.

Towards the end of the decade (1998-1999), low interest rates paved the way for companies with questionable business models to attract investors, pushing the bubble higher and higher until it popped in November of 2000.

So, let’s talk about the path to recovery for a pretend investor who invested completely in the S&P 500 Total Return Index right before the decline.

(Not every investor is completely in an S&P 500 index fund… this example just allows me to paint with a broad brush for educational purposes in this blog),

Below is a chart of a hypothetical $10,000 investment made in November 2000… It took until March 15, 2006 for this investor to get back above $10,000.

See for yourself:

November 2000 through March 2006 (5.5 years) is a long time to wait for a portfolio to completely recover, I get it. But the market did recover. Let’s hope this current crisis doesn’t end up as bad as the Tech Bubble.

Scenario #2: The Financial Crisis

The 2008 Financial Crisis was the 2nd worst economic disaster we’ve faced (only to be outdone by The Great Depression).

If you need a good recap of the crisis, I recommend reading the book or watching the movie The Big Short to get a sense of things.

From an investment perspective, let’s do the same thing we did above; let’s look at how long it would have taken a pretend investor to get back to their pre-crash levels.

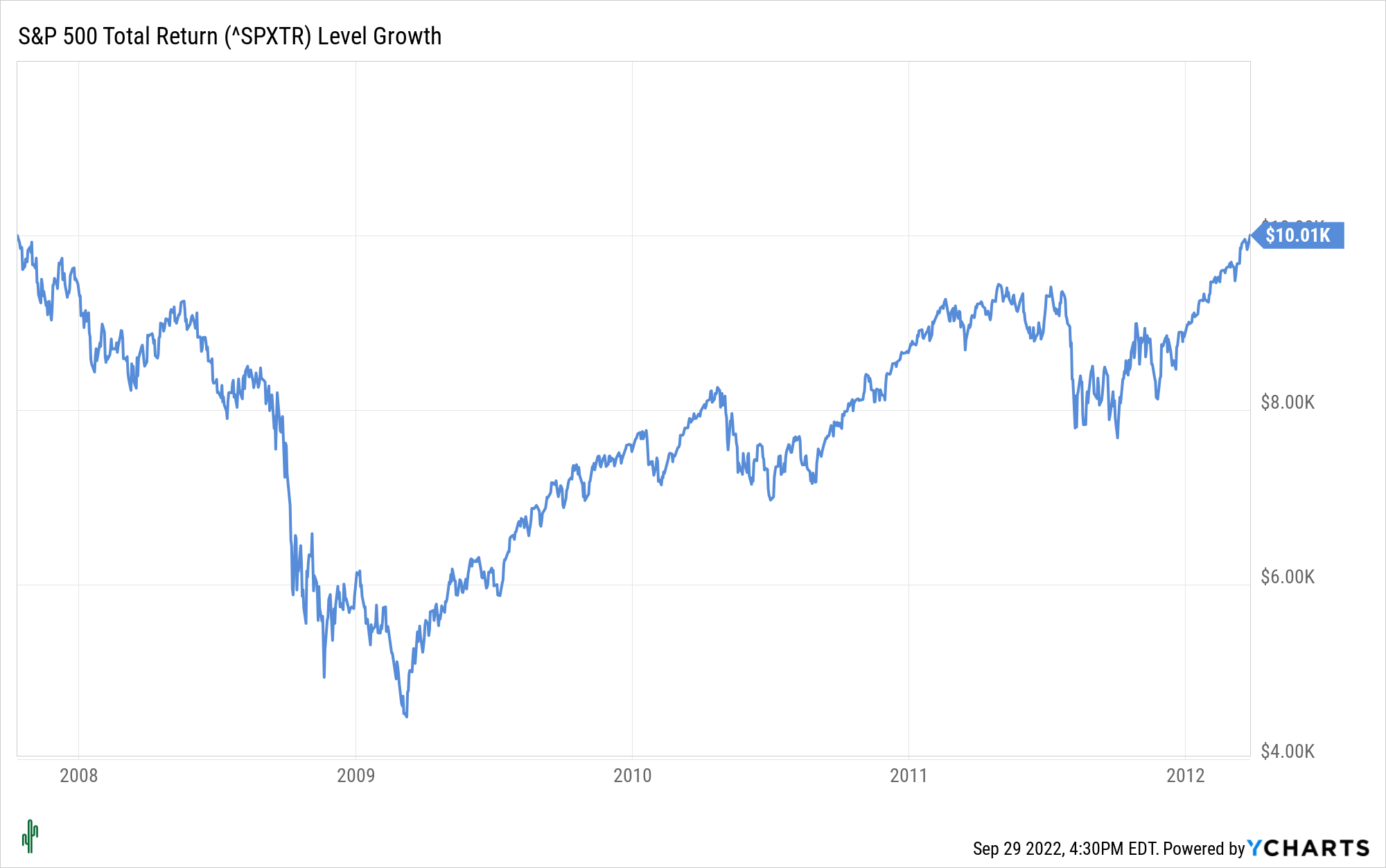

Below is a chart showing a hypothetical $10,000 investment made into the S&P 500 Total Return Index on October 12, 2007 right before the market took a swing downward. This investment finally made its way back to $10,000 on March 15, 2012.

Okay, so in this case it took about 4.5 years for the hypothetical investor to recover; not as long as it took to recover from the Tech Bubble, but still a long time.

How Do Those Prior Environments Relate to Today?

The Tech Bubble saw peak drawdown (top to bottom) of 44.2% and the Financial Crisis saw a 55.1% drawdown (for the S&P 500 Total Return index. It was far worse for the NASDAQ).

Today we’re sitting at a 23.2% drawdown on the S&P 500 Total Return Index.

(and before you jump in and use this to suggest this means we’re definitely going to see a lower drop to better mirror those prior drops, just note that the two examples above are the exceptional declines. Most 20% drops don’t reach down to 44% and 55% like these two environments.)

For an investment to lose 23.2% it needs to subsequently gain 30.2% to get back to even, and one thing is absolutely certain: I have no idea whether the stock market will gain or lose in the next few months, and I definitely don’t know specifically how long it will take to make back 30.2%.

But the good news is that I don’t need to know how long it will take, And while I almost always feel good about buying and recommending stocks after a 23% drop, I can use a different method (with less uncertainty) to help put context to this situation.

Circled below are the yields of various US government treasury securities. You’ll notice how they start to hover around 4% from 6 month maturities and onward. We haven’t seen yields this high this for about 15 years.

Many people refer to US Treasuries as “risk-free”. I don’t necessarily agree that they’re without risk (inflation can hurt them, credit could become an issue, etc.) but the payouts have historically been dependable…. If we assume an investor lost 23.2% in a 100% stock portfolio, then completely changed their risk tolerance and bought 100% treasuries yielding 4%, how long would it be until they recover?

The answer: about 6.7 years (assuming the interest was also reinvested at 4%).

I’m certainly not advocating for anyone to put all of their money in treasuries. But I will point out that yields on ‘safe stuff’ have gotten better, buying stocks after a +20% drop has typically been a good idea, and even at a 4%/yr return, it would take less than 7 years to recover from these losses.

That’s right, 6.7 years.

In an uncertain world, we can earmark this 6.7 year figure and then ask ourselves some different questions, like:

Do stock market investors get compensated for taking more risk than 4% bond market investors?

My answer: Yea, over the long run this argument holds up. Stocks have historically delivered higher returns than bonds because there is a greater risk that, if the company fails, all of the stockholders' investment will be lost (unlike bondholders who might recoup fully or partially the principal of their lending). Thus, anyone offering to own a company rather than lend money to one is typically going to demand higher returns for adopting that risk.

What if interest rates go up? Could I get higher potential yields and recover faster?

My answer: Again, yes. Or maybe interest rates come back down because inflation cools off due to improved supply chain efficiency, more energy coming online (a Ukraine peace deal maybe?), or a softening labor market… And if that happens, then you'll gladly accept lower bond market yields because the stock market would likely applaud lower rates (assuming a diversified portfolio of stocks and bonds).

The last thing I want this to sound like is a guarantee. It’s not. Instead, this is a framing of a potential way out, an ejection seat.

But if you have a good plan and a good portfolio, I’m not convinced that you need to be making big adjustments in the middle of chaotic markets. You can stay on the jet, keep your parachute packed, and not eject unnecessarily.

Lastly, whatever age you are, I promise you there has never been a younger version of your current age. Plan on having the opportunity to look back at younger versions of yourself and say “I’m glad he/she stayed the course”. That’s what an 80 year old today would be telling their 66 year old self when the stock market is was crashing in 2008, and I truly believe it’s what you’ll wish you’d told yourself in 2030 (or whatever) when you look back at 2022.

That’s all for this week.

Onward,

Adam Harding CFP

*for informational purposes only. Not investment advice. Past performance not indicative of future results. Not an offer or recommendation. Here’s a recommendation though: eat your vegetables, exercise, recycle, and spend time with your family and friends.