How to Vote

Midterms are today, so I’m going to tell you how to vote.

Oh, wait, maybe I should clear that up. As far as your candidates go, you’re more than equipped to set your own priorities and vote accordingly — I’m going to tell you how to vote with your dollars.

Let’s go.

First, a preface and acknowledgment.

My son is scared of the dark. No one taught him to be, we didn’t watch a scary movie or read a book about being scared of the dark, he just is.

Other parents — and perhaps adults too — would think this is pretty understandable; “the dark” is a thing that sometimes scares people.

Innate scary Things like this are common: the dark, snakes, spiders, uncertainty, a Federal Reserve hiking rates faster than any time in history… If you’re one of the people who’s not scared of the Thing that’s okay, but most of us are.

So if you’re concerned about how elections might impact you and your money as you venture into the future, I get it. It represents The Unknown. It’s like my son entering into a dark room… Let’s flick on a light.

Predict-shuns.

Before the 2016 Presidential election, Ray Dalio, head of the world's largest hedge fund (Bridgewater Associates) predicted market drops of at least 10% should Donald Trump win the presidency. Instead, the Dow Jones Industrial Average rose 9% from November 8th, 2016 (Election Day) through the end of 2016 and 30.62% over the following year (11/8/206 to 11/8/2017).

When Dalio speaks, people tend to listen… Hopefully they didn’t act.

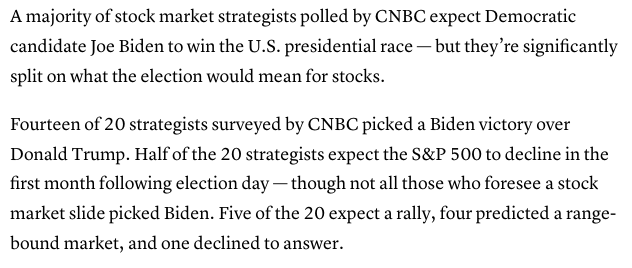

When the 2020 Election came around, the same old predictors were back at it. Here’s a snip from a CNBC article:

The stock market (DJIA) rose 11.7% from November 3rd, 2020 (Election Day) through the end of 2020.

Here’s my point:

Predictions are pretty useless as a guide for making investment decisions. Shun them. (see “Prect-shuns”, get it?)

Stocks Aren’t Congress.

The examples above were about the last two presidential elections, so what about midterms?

Well, nearly a century of US stock market returns suggests that making investment decisions based on control of the chambers of Congress is unlikely to lead to better investment outcomes.

See for yourself:

From 1926 to 2022, stocks trended higher regardless of whether Democrats or Republicans controlled the House and the Senate, or whether control was mixed.

Of course, the actions taken by Congress may impact markets, but geopolitical events (war in Ukraine, tensions with China, etc.), interest rate changes (the Fed), and Black Swan events (Enron/Worldcom/Lehman Collapse/etc.) do too. Treat the election’s impact on markets the same way you’d treat any other unpredictable event — with some apathy (as it pertains to your dollars invested in stocks).

Remember, stock investors buy companies, not a political party. Those companies focus on serving their customers and growing their businesses so they can create profits for their shareholders.

In many ways, perhaps the most attractive part of stock investing is how separated it is from what happens in Washington. Companies are agile — they figure out how to thrive in a dynamic world. Lean into that.

How to Vote with Your Dollars

If you’re like me then you’re receiving dozens of political calls and texts each day, your mailbox is full of political junk mail, and ads on your TV are more of the same. You’re getting bombarded because people want your vote and they’re competing for it.

Similarly your dollars are facing competition as well and, for the first time in several years, the competition between stocks and bonds is up for debate. Of course, I can’t tell you specifically what to do in a blog format (book a chat for that kind of discussion), but let me frame some concepts to see if I can help.

But first a story:

In January you walk into a store and see the most perfect avocado for $3. You think to yourself, what could $3 get me that I’d like more than an avocado? The $3 generates virtually no interest sitting in your high yield checking account, stocks are volatile, the real estate market is too competitive, and avocados are way more delicious than the other stuff at the store. You buy it.

In this story, the avocado is the hero (or perhaps your love interest… bear with me, I’m making this up on the fly), but there’s also a villain in this story:

The Federal Reserve.

And the Federal Reserve DOES NOT WANT YOU TO BUY THAT AVOCADO!

Someone stocked that avocado on the shelves, someone helped you at checkout, someone is doing the bookkeeping for the store, etc. and they’re all earning paychecks — and those paychecks are contributing to inflation because those gosh darn workers are out there living their lives. So the Fed wants to destroy your demand for avocados to help get them all fired (which is pretty messed up if you ask me…seems like they could, you know, try to figure out a way to boost avocado production to help put downward pressure on prices).

So how are they getting people fired —er, I mean, softening the labor market?

Well, the yield on a one month US Treasury security is up 6,150% (!!!) thus far in 2022. Seriously, in January you could buy a 1-month bill and it would pay about 0.04%/yr and today the yield is 3.75%. Even the yield on the Schwab Value Advantage Money Market Fund (SWVXX) is up to 3.30% (link). This is what happens when the Fed ticks up the Federal Funds rate.

Today you have to remember that the $3 can generate a meaningful yield in your money market or bond funds. For the first time in more than a decade, saving in ‘safe stuff’ is starting to look more attractive than buying all of the avocados (or whatever).

How to Vote Lesson #1: Think about the opportunity cost of short term buying decisions.

Despite my disgruntled feelings about the Fed action, you should use their approach to your benefit and start squeezing yield out of your short term investments.

But there’s more than just avocados, treasuries, or money market funds — in fact, there’s something called an equity premium.

“Equity premium” is just a fancy way to say “stocks tend to outperform bonds.” Of course, stocks don’t always outperform bonds because nothing always outperforms anything else.

To capture this potential outperformance, an investor typically needs two things: time and discipline.

If your objectives are long term (like retire in 10 years, or send our kids to college in 13 years, or retire in 5 years but we don’t need to draw from our investments right away, etc.) then you might buy some stocks. But if every drop in the market causes you to freak out like a 3 year old who’s scared of the dark (again, understandably), then maybe you don’t have the discipline to pursue the equity premium.

Dave Ramsey is pretty famous for suggesting that investors only buy “good growth stock mutual funds” and he tends to get quite a bit of blowback from the traditional finance community for eschewing bonds when giving this advice. Honestly, his point is not that controversial as he’s basically saying; if you have time on your side and the stomach to tolerate risk, invest in the thing with the best chance for growth….. And that thing is stocks. Eugene Fama calls it an “Equity Premium” and got a Nobel Prize for saying basically the same thing.

Even more, the S&P 500 index is down more than 20% YTD. Go back and look at every other time when the stock market was down 20% and see if it would have been a good time to buy. I’ll leave that evaluation up to you, but I’d bet you can guess where I stand.

How to Vote Lesson #2: Think about the opportunity presented for long term investing decisions.

Things get tricky when you’re not sure how much risk you can tolerate, when you maybe don’t have 10 years or more to invest, or when you’re retiring and you need some funds right now and you also need your money to last 20-30 years into retirement. That’s where we typically come in to help people work around these more nuanced discussions.

Wrapping Up.

I spend a lot of time paying attention to the opinions of brilliant investing minds (people like Warren Buffett, Ray Dalio, Jeff Gundlach, and Jeremy Grantham to name a few). Because their audiences demand it, they also tend to make bold predictions about how events will impact markets. I make it a point to remember what the prediction was and how well it fared — often quite poorly.

You see, even the most well-conceived narratives fail spectacularly most of the time, but time tends to forgive those who make predictions as they bury the incorrect ones and bring to the forefront the few-and-far between accurate palm-readings.

I’d never claim to be smarter than any of those famous investors — but I might be more comfortable saying less-sensationalistic things and being a bit more boring.

Thus, I’m here to deliver a different message:

What happens in November of 2022 isn’t likely to make as much of an impact on your money as you think it might. Especially when we compare the uncertain impact of elections on markets with the relatively certain positive impact we can make by making some prudent financial planning moves (like tax loss harvesting, swapping mutual funds for ETFs to avoid capital gains distributions, maximizing 401k/403b contributions before year-end, and considering Roth IRA conversions).

For me it’s clear what we should do as a result of the elections: the same things we do every year in November and December. For clients, this involves booking a tax-planning meeting. If you’re not a client, feel free to reach out to see if we can help (email adam@hardingwealth.com).

Until next time, onward.

Adam Harding

CFP | Advisor & Founder @ Harding Wealth | Smartvestor Pro | Dad

Ps…. No darkness is getting these kids while I’m around.